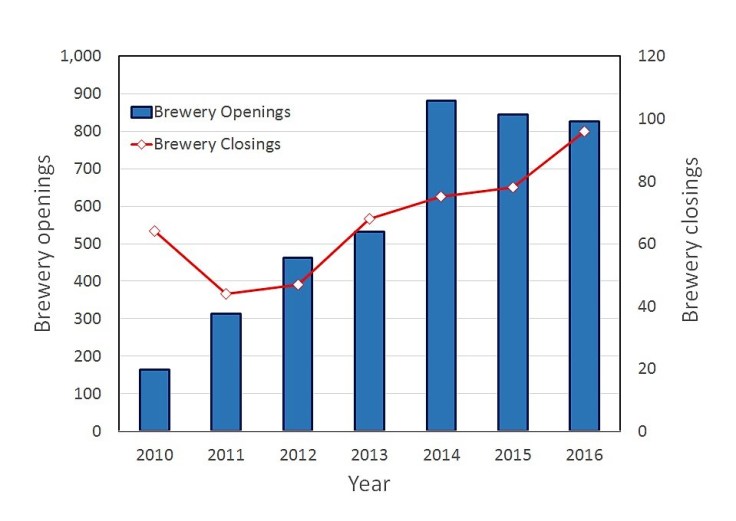

After years of unbridled growth, the American craft beer industry appears to be entering a new phase. Over 800 craft breweries opened their doors in 2016, but the rate at which they are opening is gradually starting to slow. A small but increasing number of breweries are closing up shop, Blank Slate Brewing in Cincinnati being an example that hits close to home for many of my readers. At the same time the multinational conglomerates like AB-InBev are acquiring mid-size breweries at an increasing clip. Several breweries that were darlings of the craft beer world when I started this blog four years ago are now owned by the big guys: Wicked Weed (AB-InBev), Lagunitas (Heineken), Ballast Point (Constellation), Devils Backbone (AB-InBev), Funky Buddha (Constellation), Terrapin (MillerCoors), and many others. Even the pioneers of the craft brewery movement are struggling. Sales at Boston Beer Company were down 5% in 2016. Sierra Nevada’s retail-store sales fell by 7.5% in the first six months of 2017, which followed a decrease of 6.9% in 2016. The first sales decline in the history of the company that invented American Pale Ales. In August America’s oldest craft brewery, Anchor Brewing, was acquired by Japanese giant Sapporo.

To get a sense of what is going on I reached out to a man who is uniquely qualified to talk about both sides of the beer industry, Jason McKibben, brewmaster and co-owner of North High Brewing in Columbus. Before joining North High, Jason spent 12 years working for Anheuser-Busch, including a stint as head brewer at the Columbus facility and another managing the research pilot brewery in St. Louis. From there he moved to Anchor Brewing in San Francisco, where he was director of production, before joining North High in 2014. Since Jason came on board North High Brewing has evolved from a small neighborhood brewery with a brew on-premises facility to a mid-size production brewery that distributes throughout Ohio. Over that same period their production volume has grown 12-fold and is on pace to hit 6000 bbl in 2017.

Jason thanks so much for taking time to answer my questions. Let me start by asking you what issues keep you awake at night?

Jason: The phenomenon of beer buyers and consumers constantly asking for something “new” has worn very thin. While it’s definitely important to stay focused on innovation, relying on “newness” to sell beer fosters gimmicks and suppresses opportunities to refine our process and craft.

That’s an interesting point and one that hits home while spending time here in Europe, where some breweries have been making the same beer for centuries. Some people think that flagship brands are on their way out in the US? How do your year-round offerings like the award winning North High Pale Ale compete with the seasonal offerings like Grapefruit Walleye?

Jason: Our core brands do not experience all that much competition with our seasonal brands. If anything, Hefeweizen is stronger in the summer and Milk Stout is stronger in the winter, but that’s core vs. core. Our seasonal brands are on a different SKU, so they’re always available side-by-side with the core. However, I do think the newness issue depresses core sales volume, especially with on-premise sales. I think the core is pretty solid right now, but we have not been around all that long, so 2018 might be the year we shake some of the core up a bit. We feel like we’ve developed some great beers as seasonals or one-offs that could really grow if they were available year-round. Time will tell.

It seems to me that larger craft breweries find themselves being squeezed from both ends. On the one hand, international conglomerates like AB InBev are applying pressure by acquiring craft breweries that compete for shelf space and tap handles, while small neighborhood breweries chip away at sales from the other end. As someone who spent 12 years at Anheuser-Busch what do you think motivates the big boys to acquire craft breweries?

Jason: The scale of the big guys has pigeon-holed them into being dependent on home runs. They aren’t nimble enough and simply don’t have the patience to wait for one of their new products to organically grow (one exception is Coors and Blue Moon). The brewers at A-B in Columbus created a Helles lager back in 2006, which was delicious. I think we brewed it twice before the sales team pulled the plug. No one gave it a chance. I don’t understand the reasoning for all of A-B’s acquisitions, but for the most part these are ready-made brands that they think can be easily scaled for a much larger distribution. Of course, some styles are easier to scale than others.

Can you expand on that point, what issues do breweries face when it comes to scale up?

Jason: When I was still with A-B, I recall reviewing a recipe for an IPA from one of their new acquisitions and wondering how we could get 1,000 lbs of hops into the whirlpool quickly enough. To date, I haven’t tasted an A-B produced IPA or other hoppy style that could compete with the contenders of craft. A-B used to have quite a substantial engineering department that may have been able to solve some of these problems with scalability, but most of their jobs were terminated when InBev took over.

Lots of beer geeks were up in arms about AB-InBev’s purchase of Wicked Weed, in large part because of the popularity of their sour beer line. It seems to me that barrel aged sour beers are among the hardest styles to scale up, though breweries like Rodenbach do make sours at a large scale. Any speculation what A-B has in mind for the sour program at Wicked Weed?

Jason: Given the complexities of scaling up and the typical pricing levels of sour beers like those at Wicked Weed, I don’t see A-B going very big with the Wicked Weed sour portfolio. The growth potential is probably not there. Of course, they have the resources to buy as many foeders and used barrels as they want and they most likely will boost the capacity Wicked Weed’s current facility to some extent. I wonder if they will mostly use the Wicked Weed sours as leverage with high end accounts that currently don’t purchase much from their local A-B distributor.

One of the most interesting theories I’ve seen on this topic is a piece by Chris Herron from Creature Comforts Brewing wrote for Good Beer Hunting. In that article he suggests that acquisitions by corporations like AB-InBev are part of a strategy designed to protect the premium status of their core brands, by minimizing the price gap between products like Budweiser/Bud Light and craft beer. What do you think of that notion?

Jason: When the recession hit in 2008, many consumers traded down to sub-premium brands like Busch and Natural Light. A-B responded by increasing pricing on those sub-premium brands to lessen the incentive to trade down. So, of course they like the margins of their premium brands. However, they should love the margins of the craft brands even more, especially at the efficiencies at which they operate. If they’re keeping their craft brands priced lower than comparable independent craft, I think it’s because they’re not selling enough and they desperately need the volume to make this endeavor work.

As the former production director for Anchor, what did you think of Sapporo’s acquisition of Anchor? Did you see something like that coming?

Jason: I’m not surprised at all. When I was at Anchor, we met with Sapporo and Suntory, but for a different reason. Anchor was developing a new brewery on Pier 48 in San Francisco and were looking to contract brew to fill out the capacity at start-up. The acquisition by Sapporo is different. The city of San Francisco, and Anchor Steam in particular, is quite popular in Asia. The brewery was routinely asked to distribute its beers in Asia, but rarely accepted due to the costs of distribution and other pricing issues. I speculate that Sapporo could brew Anchor Steam in Japan and move a tremendous amount of beer in China.

Small neighborhood breweries seem to be thriving. According to statistics from the Brewers Association, 76% of the 5000+ breweries in the US produce less than 1000 bbl per year. They can be agile, serve über-fresh beer, and develop a rapport with their customers in a way that is difficult for breweries with a big distribution footprint to replicate. In Bart Watson’s (Chief Economist for the Brewers Association) speech at the Ohio Brewers Conference he mentioned a Nielson survey that found 67% of craft beer drinkers and 45% of all beer drinkers said the descriptor “local” played an important role in their purchasing decisions. What do you think defines a beer as local? Is North High Brewing considered local in Cincinnati, Cleveland, or Toledo?

Jason: The local movement is a generation-altering consumer trend that is much bigger than just the beer industry. It’s affecting every industry. I don’t have a good definition of local for the beer industry. Maybe it’s any brewery that one could easily visit during the course of a normal day. I do think many Ohioans view any Ohio brewery with preference over those from other states. I also think many other Ohioans are swayed by good marketing from wherever it originates. I don’t think North High is viewed as local outside of central Ohio, but our salespeople do leverage our Ohio credentials in other Ohio markets.

What do you think about the Brewer’s Association recent launch of the Independent logo? Is North High Brewing going to use the logo?

Jason: The BA has taken on a life of its own and has become a brand unto itself. The Independent logo is fine. The BA does some fine stuff. Bart Watson is a very smart and competent economist. Paul Gatza’s mullet is absolutely killer. Maybe the new Independent logo is an admission that the BA has butchered the definition of “Craft” beyond all recognition. I don’t expect to put the Independent logo on our cans. The logo of the Ohio Craft Brewers Association will appear on our cans much sooner.

Leave a comment